In the previous articles we looked at how to calculate different types of synergy. In this article we will delve into cost synergies.

As we explained in the previous blog posts, Cost synergies are those that mergers bring about by combining, eliminating or streamlining redundant processes. They are easier to predict as they are calculated based on the current spending of both organizations in specific areas such as IT, sales and marketing, etc. Unlike the general perception that cost synergies are only associated with RIF (reduction in force), there are many other forms of cost synergies such as IT consolidation, reduced S&M spending and renegotiated agreements that may not necessarily require such measures. Some examples of cost synergies are:

- Reducing staff headcount by identifying functional duplication

- Reducing rent by consolidating offices and other locations

- Consolidating suppliers or renegotiating supplier terms

- Increasing utilization of capital assets such as factories, transportation etc.

- Reducing professional services fees

Even though cost synergies are less speculative than revenue synergies, it is important to model and implement them properly. Factors such as the source of the synergies, the time to implement and the cost to implement them are important considerations. Moreover, unlike common perception of cost synergies being a fixed one time or recurring benefit, they could exhibit growth over time much like revenue synergies in some scenarios.

Cost synergies can be classified in one of two categories:

- Fixed costs – Costs that do not change irrespective of the sales volume

- Variable costs – Costs that change proportional to the sales volume

Modeling fixed and variable costs helps determine the total profitability.

Fixed cost synergies

Fixed costs are expenses incurred independent of any business activities. These are costs that are indirect and don’t apply to a company’s sales, production of goods or services.

Examples of fixed costs are:

- Rent/lease payments or mortgage.

- Salaries.

- Insurance.

- Equipment lease payment.

- Car lease payment.

- Utility payments.

- Phone service.

- Business insurance.

Variable cost synergies

Variable costs are expenses that change in proportion to how much a company produces a product or sells. They rise as sales increase and fall as sales drop. Therefore, it is a bit more difficult to determine their value over time.

Examples of variable costs are:

- CAC – Customer acquisition cost

- CLTV – Customer LifeTime Value

- CCR – Customer Conversion Ratio

- COGS – Cost of Goods

- Raw material and inputs to production

- Packages, wages, commissions

- Some utilities tied to the production capacity

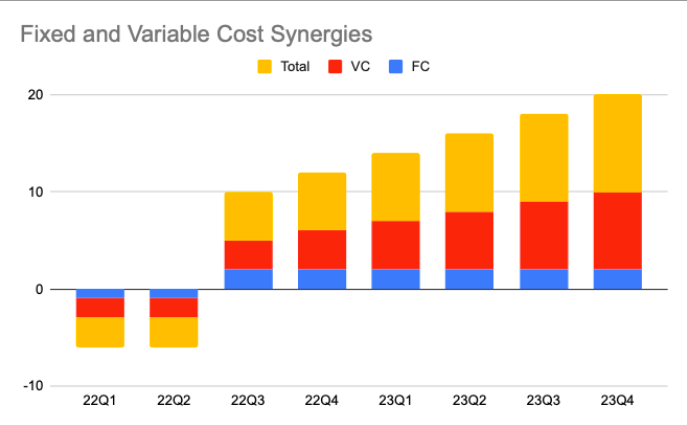

Cost synergies in component view

In the component framework, the formula for cost synergies can be stated as:

Cost synergy value = Sum over all quarters [FC(t) + VC(t) ]

FC = Fixed cost synergies

VC = Variable cost synergies

Antagonism factors must be taken into consideration when drawing a timeline for cost synergies. These items can help you plan for a more effective planning to exploit the benefits. Here are a few examples of such factors:

- Lack of cultural fit

- Overextending resources

- External factors

- Lack of management focus

- Lack of morale

- Gap in compensation and benefits

The following diagram demonstrates the two types of synergies and their impact on the overall synergy.:

In this article we discussed two variants of cost synergies. In a future article we will take a closer look at modeling revenue synergies.